تم الحل ✓

categoryتمويل ومصارف

schoolبكالوريوس

event_available2026-07-14

السؤال

Transcribed Image Text:

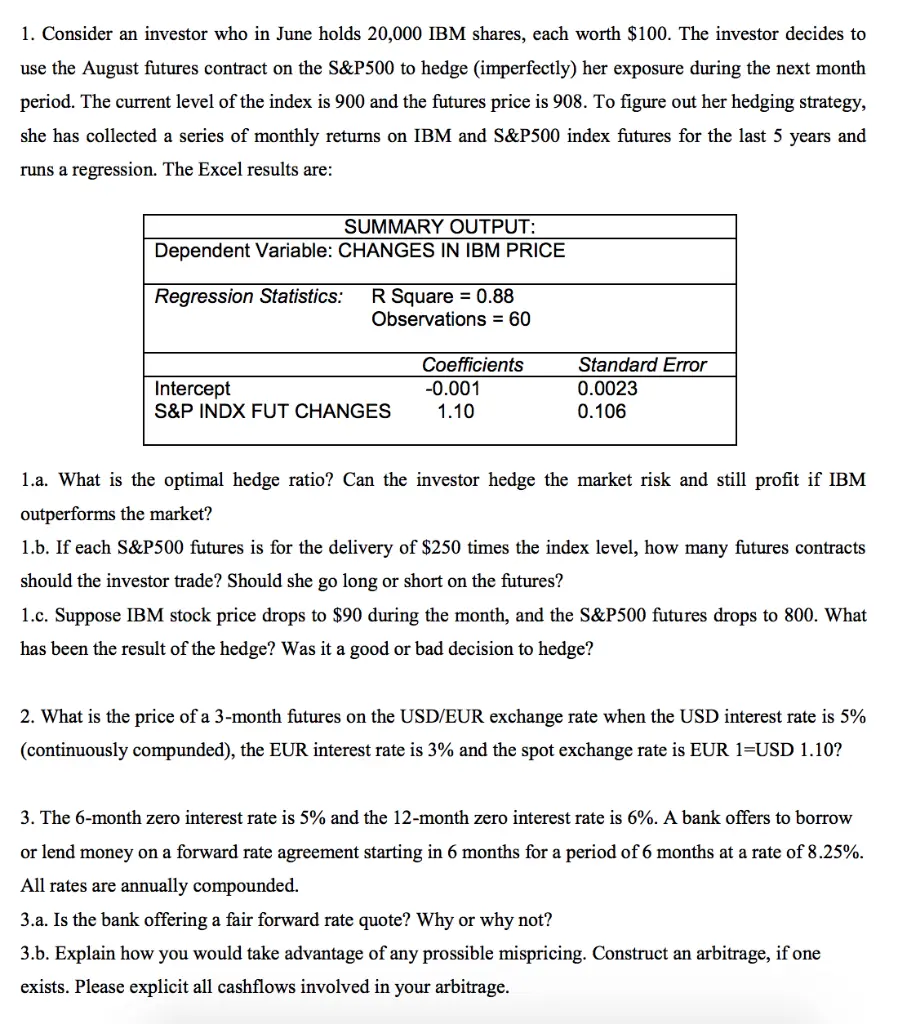

1. Consider an investor who in June holds 20,000 IBM shares, each worth $100. The investor decides to

use the August futures contract on the S&P500 to hedge (imperfectly) her exposure during the next month

period. The current level of the index is 900 and the futures price is 908. To figure out her hedging strategy,

she has collected a series of monthly returns on IBM and S&P500 index futures for the last 5 years and

runs a regression. The Excel results are:

SUMMARY OUTPUT:

Dependent Variable: CHANGES IN IBM PRICE

Regression Statistics: R Square 0.88

Observations = 60

Coefficients

Intercept

-0.001

Standard Error

0.0023

S&P INDX FUT CHANGES

1.10

0.106

1.a. What is the optimal hedge ratio? Can the investor hedge the market risk and still profit if IBM

outperforms the market?

1.b. If each S&P500 futures is for the delivery of $250 times the index level, how many futures contracts

should the investor trade? Should she go long or short on the futures?

1.c. Suppose IBM stock price drops to $90 during the month, and the S&P500 futures drops to 800. What

has been the result of the hedge? Was it a good or bad decision to hedge?

2. What is the price of a 3-month futures on the USD/EUR exchange rate when the USD interest rate is 5%

(continuously compunded), the EUR interest rate is 3% and the spot exchange rate is EUR 1=USD 1.10?

3. The 6-month zero interest rate is 5% and the 12-month zero interest rate is 6%. A bank offers to borrow

or lend money on a forward rate agreement starting in 6 months for a period of 6 months at a rate of 8.25%.

All rates are annually compounded.

3.a. Is the bank offering a fair forward rate quote? Why or why not?

3.b. Explain how you would take advantage of any prossible mispricing. Construct an arbitrage, if one

exists. Please explicit all cashflows involved in your arbitrage.

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.