تم الحل ✓

categoryرياضيات

schoolبكالوريوس

event_available2026-07-14

السؤال

Transcribed Image Text:

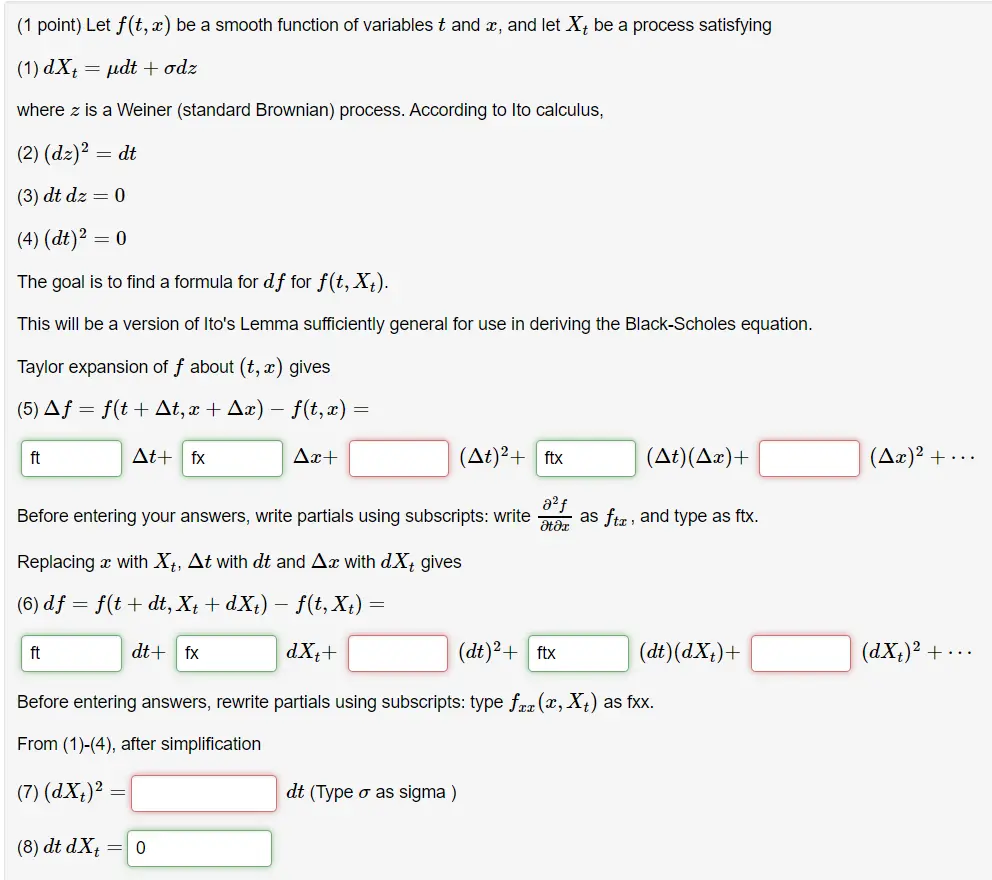

(1 point) Let f(t, x) be a smooth function of variables t and x, and let ✗+ be a process satisfying

(1) dX+udt + odz

=

where z is a Weiner (standard Brownian) process. According to Ito calculus,

(2) (dz)² = dt

(3) dt dz = 0

(4) (dt)²

= 0

The goal is to find a formula for df for f(t, Xt).

This will be a version of Ito's Lemma sufficiently general for use in deriving the Black-Scholes equation.

Taylor expansion of f about (t, x) gives

(5) Aƒ = f(t + At, x + Ax) − f(t, x) =

=

ft

At+ fx

Ax+

(At)²+ ftx

(At)(Ax)+

(Ax)² + ...

Before entering your answers, write partials using subscripts: write

as fta, and type as ftx.

Ətəx

Replacing a with Xt, At with dt and Ax with dX+ gives

(6) df = f(t + dt, Xt + dxt)

ft

dt+ fx

-

f(t, Xt) =

=

dx++

(dt)²+ ftx

(dt) (dX+)+

(dX+)² + ...

Before entering answers, rewrite partials using subscripts: type frx (x, X+) as fxx.

From (1)-(4), after simplification

(7) (dX+)²

(8) dt dXt

= 0

dt (Type σ as sigma)

Now using (1), (4), (7) and (8), equation (6) reduces to

(9) df =

Type μ as mu, σ as sigma.

dt+

dz

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.