تم الحل ✓

categoryرياضيات

schoolبكالوريوس

event_available2026-07-14

السؤال

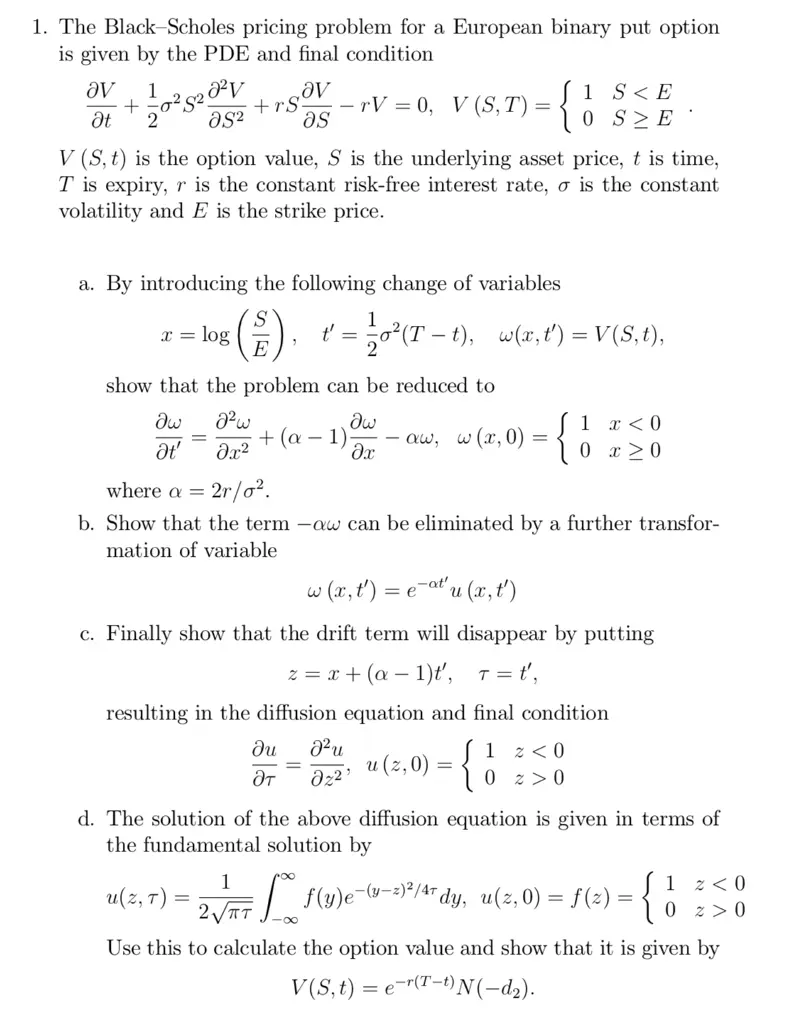

Transcribed Image Text:

1. The Black-Scholes pricing problem for a European binary put option

is given by the PDE and final condition

av 1

+ 02 82

Ət 2 მS2

+rS -rV=0, V (S,T) =

1 S<E

av

as

0 SE

V (S,t) is the option value, S is the underlying asset price, t is time,

T is expiry, r is the constant risk-free interest rate, σ is the constant

volatility and E is the strike price.

a. By introducing the following change of variables

x = log

E

t' = ½ o² (T− t), w(x,t) = V(S,t),

show that the problem can be reduced to

θω

J²w

θω

+ (a

1)

მე2

- αω,

ω

дх

; (x, 0) = {

1 x <0

0x0

It'

=

where a = 2r/02.

b. Show that the term -aw can be eliminated by a further transfor-

mation of variable

-at'

น

w(x, t') = e¯atu (x, t')

c. Finally show that the drift term will disappear by putting

z=x+(a1)t', T=t',

resulting in the diffusion equation and final condition

ди J²u

Эт

Oz2

и

(2,0)

1 <0

=

0 z>0

d. The solution of the above diffusion equation is given in terms of

the fundamental solution by

1

u(z,T)

=

= f(y)e-(-2)²³/4 dy, u(2, 0) = ƒ (²) =

1

2<0

2√7

пт

0 20

Use this to calculate the option value and show that it is given by

V(S,t) er(T-)N(-d₂).

=

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.