تم الحل ✓

categoryرياضيات

schoolبكالوريوس

event_available2026-07-14

السؤال

Transcribed Image Text:

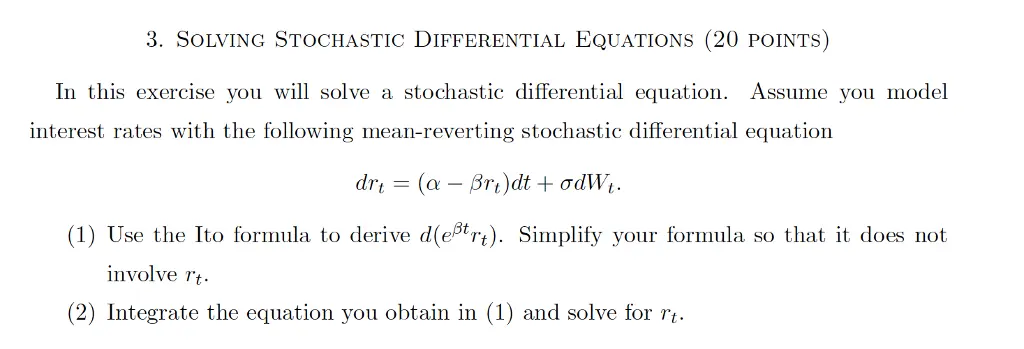

3. SOLVING STOCHASTIC DIFFERENTIAL EQUATIONS (20 POINTS)

In this exercise you will solve a stochastic differential equation. Assume you model

interest rates with the following mean-reverting stochastic differential equation

drt (a Brt)dt + σdWt.

=

(1) Use the Ito formula to derive d(ert). Simplify your formula so that it does not

involve rt.

(2) Integrate the equation you obtain in (1) and solve for rt.

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.