تم الحل ✓

categoryتمويل ومصارف

schoolبكالوريوس

event_available2026-07-14

السؤال

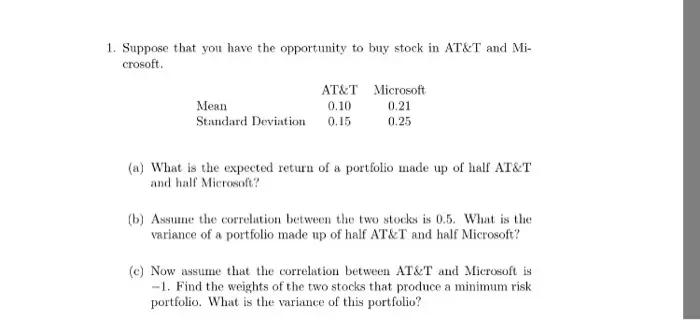

Transcribed Image Text:

1. Suppose that you have the opportunity to buy stock in AT&T and Mi-

crosoft.

AT&T Microsoft

Mean

0.10

0.21

Standard Deviation 0.15

0.25

(a) What is the expected return of a portfolio made up of half AT&T

and half Microsoft?

(b) Assume the correlation between the two stocks is 0.5. What is the

variance of a portfolio made up of half AT&T and half Microsoft?

(e) Now assume that the correlation between AT&T and Microsoft is

-1. Find the weights of the two stocks that produce a minimum risk

portfolio. What is the variance of this portfolio?

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.