تم الحل ✓

categoryتمويل ومصارف

schoolبكالوريوس

event_available2026-07-14

السؤال

Transcribed Image Text:

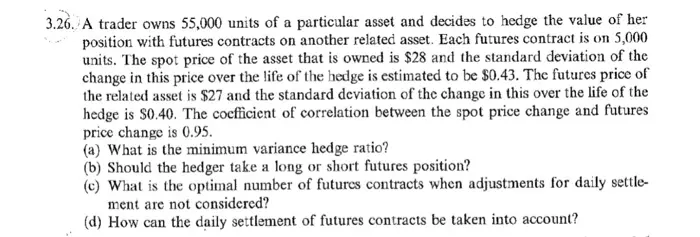

3.26. A trader owns 55,000 units of a particular asset and decides to hedge the value of her

position with futures contracts on another related asset. Each futures contract is on 5,000

units. The spot price of the asset that is owned is $28 and the standard deviation of the

change in this price over the life of the hedge is estimated to be $0.43. The futures price of

the related asset is $27 and the standard deviation of the change in this over the life of the

hedge is $0.40. The coefficient of correlation between the spot price change and futures

price change is 0.95.

(a) What is the minimum variance hedge ratio?

(b) Should the hedger take a long or short futures position?

(c) What is the optimal number of futures contracts when adjustments for daily settle-

ment are not considered?

(d) How can the daily settlement of futures contracts be taken into account?

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.