تم الحل ✓

categoryتمويل ومصارف

schoolبكالوريوس

event_available2026-07-13

السؤال

Transcribed Image Text:

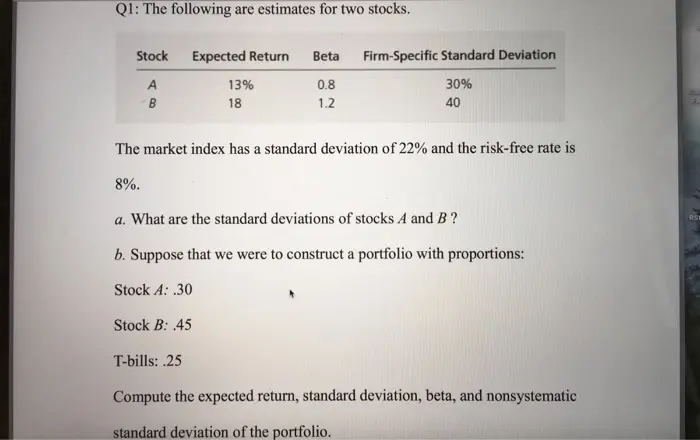

Q1: The following are estimates for two stocks.

Stock

Expected Return

Betal

Firm-Specific Standard Deviation

A

13%

0.8

30%

B

18

1.2

40

The market index has a standard deviation of 22% and the risk-free rate is

8%.

a. What are the standard deviations of stocks A and B?

b. Suppose that we were to construct a portfolio with proportions:

Stock A: .30

Stock B: .45

T-bills: .25

Compute the expected return, standard deviation, beta, and nonsystematic

standard deviation of the portfolio.

ASW

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.