تم الحل ✓

categoryإحصاء

schoolبكالوريوس

event_available2026-07-13

السؤال

Transcribed Image Text:

-

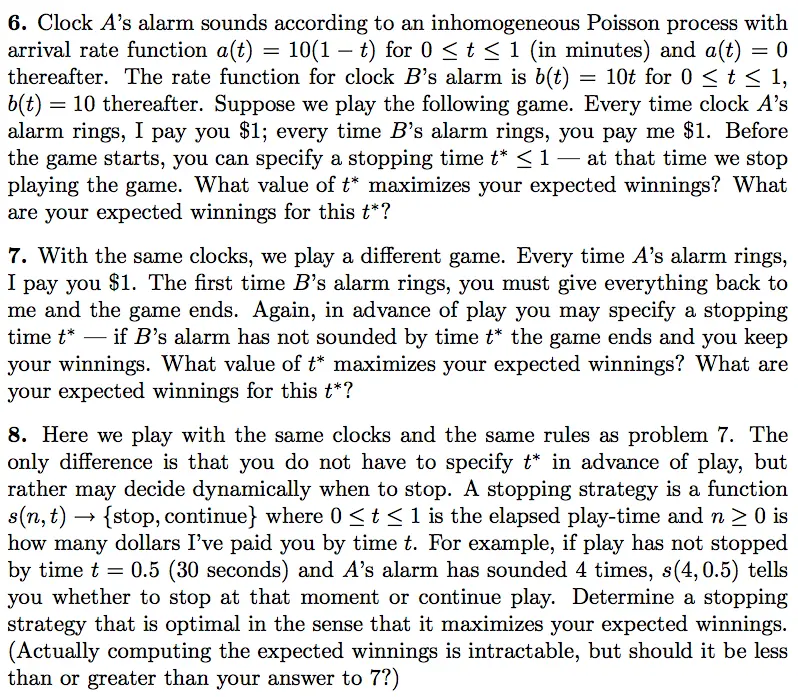

6. Clock A's alarm sounds according to an inhomogeneous Poisson process with

arrival rate function a(t) = 10(1 − t) for 0 ≤ t≤ 1 (in minutes) and a(t) = 0

thereafter. The rate function for clock B's alarm is b(t) = 10t for 0 ≤ t≤ 1,

b(t) =

= 10 thereafter. Suppose we play the following game. Every time clock A's

alarm rings, I pay you $1; every time B's alarm rings, you pay me $1. Before

the game starts, you can specify a stopping time t* <1 at that time we stop

playing the game. What value of t* maximizes your expected winnings? What

are your expected winnings for this t*?

-

7. With the same clocks, we play a different game. Every time A's alarm rings,

I pay you $1. The first time B's alarm rings, you must give everything back to

me and the game ends. Again, in advance of play you may specify a stopping

time t* if B's alarm has not sounded by time t* the game ends and you keep

your winnings. What value of t* maximizes your expected winnings? What are

your expected winnings for this t*?

8. Here we play with the same clocks and the same rules as problem 7. The

only difference is that you do not have to specify t* in advance of play, but

rather may decide dynamically when to stop. A stopping strategy is a function

s(n,t). →> {stop, continue} where 0 <t≤1 is the elapsed play-time and n ≥ 0 is

how many dollars I've paid you by time t. For example, if play has not stopped

by time t = 0.5 (30 seconds) and A's alarm has sounded 4 times, s(4,0.5) tells

you whether to stop at that moment or continue play. Determine a stopping

strategy that is optimal in the sense that it maximizes your expected winnings.

(Actually computing the expected winnings is intractable, but should it be less

than or greater than your answer to 7?)

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.