تم الحل ✓

categoryإحصاء

schoolبكالوريوس

event_available2026-07-13

السؤال

Transcribed Image Text:

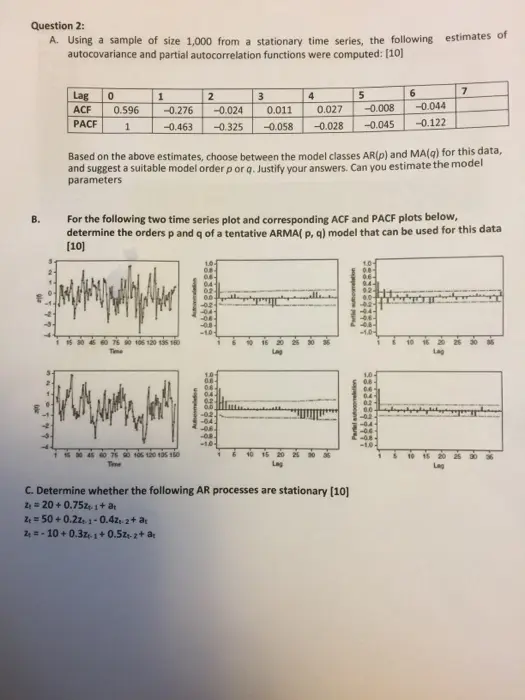

Question 2:

A. Using a sample of size 1,000 from a stationary time series, the following estimates of

autocovariance and partial autocorrelation functions were computed: [10]

Lag

ACF

0

1

2

3

4

5

6

7

0.596

PACF

1

-0.276

-0.463 -0.325 -0.058

-0.024

0.011

0.027

-0.008

-0.044

-0.028

-0.045

-0.122

B.

Based on the above estimates, choose between the model classes AR(p) and MA(q) for this data,

and suggest a suitable model order p or q. Justify your answers. Can you estimate the model

parameters

For the following two time series plot and corresponding ACF and PACF plots below,

determine the orders p and q of a tentative ARMA( p, q) model that can be used for this data

[10]

10-

08-

06-

04-

02-

0.0-

-08-

-0.8-

-10-

90 106 120 136 160

25 30 36

Timme

02.

-08-

-1.0-

90 106 120 135 150

Time

6

C. Determine whether the following AR processes are stationary [10]

Z₁ = 20 +0.752.1+ a

ze 50+0.2z-1-0.42-2+ at

2-10+0.3z-1+0.5z+-2+ a

02-

1.0-

0.8-

Lag

25 30 35

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.