تم الحل ✓

categoryتمويل ومصارف

schoolبكالوريوس

event_available2026-07-13

السؤال

Transcribed Image Text:

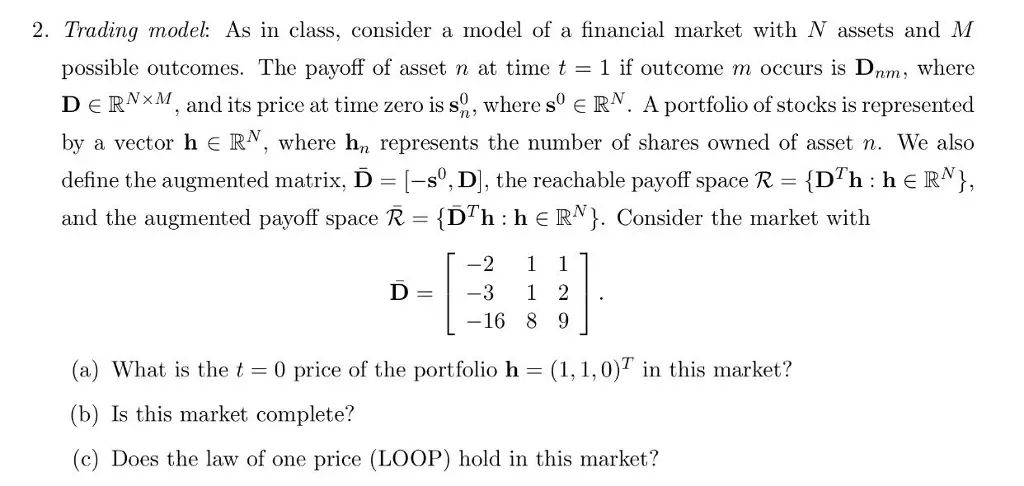

2. Trading model: As in class, consider a model of a financial market with N assets and M

possible outcomes. The payoff of asset n at time t = 1 if outcome m occurs is Dnm, where

DERNXM, and its price at time zero is so, where sº ERN. A portfolio of stocks is represented

by a vector h = RN, where h₂ represents the number of shares owned of asset n. We also

define the augmented matrix, D = [-sº, D], the reachable payoff space R = {DTh: hЄRN},

and the augmented payoff space R = {DTh: hЄRN}. Consider the market with

-2

1 1

Ꭰ =

-3 1 2

-16 8 9

(a) What is the t = 0 price of the portfolio h = (1,1,0) in this market?

(b) Is this market complete?

(c) Does the law of one price (LOOP) hold in this market?

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.