تم الحل ✓

categoryالاقتصاد والأعمال

schoolبكالوريوس

event_available2026-07-15

السؤال

Transcribed Image Text:

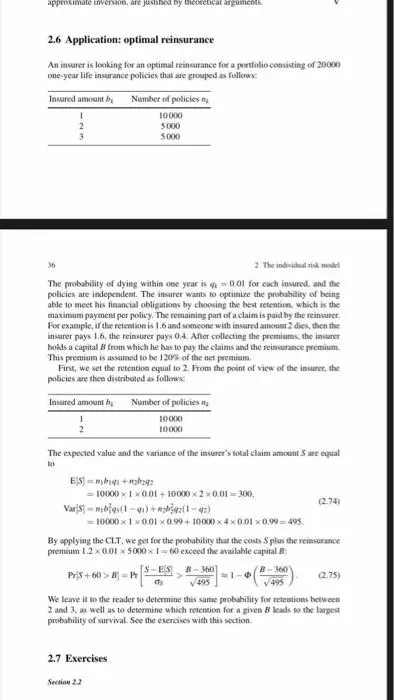

approximate inversion, are justified by theoretical arguments.

2.6 Application: optimal reinsurance

An insurer is looking for an optimal reinsurance for a portfolio consisting of 20000

one-year life insurance policies that are grouped as follows:

Insured amount by

Number of policies

10000

2

3

5000

5000

36

2. The individual risk model

The probability of dying within one year is 0.01 for each insured, and the

policies are independent. The insurer wants to optimize the probability of being

able to meet his financial obligations by choosing the best retention, which is the

maximum payment per policy. The remaining part of a claim is paid by the reinsurer.

For example, if the retention is 1.6 and someone with insured amount 2 dies, then the

insurer pays 1.6, the reinsurer pays 0.4. After collecting the premiums, the insurer

holds a capital B from which he has to pay the claims and the reinsurance premium

This premium is assumed to be 120% of the net premium.

First, we set the retention equal to 2. From the point of view of the insurer, the

policies are then distributed as follows:

Insured amount by Number of policies n

1½

10000

10000

The expected value and the variance of the insurer's total claim amount S are equal

to

ES

+2

= 10000 × 1 × 0.01+10000×2×0.01 = 300,

Vars=b(1-4)+2(1-42)

=10000x 1 x 0.01 x 0.99+10000x4x0.01 x 0.99-495.

(2.74)

By applying the CLT, we get for the probability that the costs S plus the reinsurance

premium 1.2x0.01 x 5000 x 1-60 exceed the available capital B

[S-ES

Pris+60>B-Pr

B-360]

√495

(B-360)

495

(2.75)

We leave it to the reader to determine this same probability for retentions between

2 and 3, as well as to determine which retention for a given B leads to the largest

probability of survival. See the exercises with this section.

2.7 Exercises

Section 2.2

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.