تم الحل ✓

categoryرياضيات

schoolبكالوريوس

event_available2026-07-15

السؤال

Transcribed Image Text:

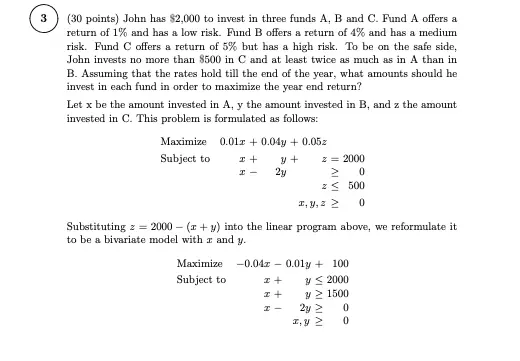

3

(30 points) John has $2,000 to invest in three funds A, B and C. Fund A offers a

return of 1% and has a low risk. Fund B offers a return of 4% and has a medium

risk. Fund C offers a return of 5% but has a high risk. To be on the safe side,

John invests no more than $500 in C and at least twice as much as in A than in

B. Assuming that the rates hold till the end of the year, what amounts should he

invest in each fund in order to maximize the year end return?

Let x be the amount invested in A, y the amount invested in B, and z the amount

invested in C. This problem is formulated as follows:

Maximize 0.01x + 0.04y+ 0.05z

Subject to

x+

3+

z=2000

エー

2y

0

<< 500

x, y,

0

Substituting z=2000-(x+y) into the linear program above, we reformulate it

to be a bivariate model with x and y.

Maximize

Subject to

-0.04x-

0.01y+100

x+

y≤2000

x +

y≥ 1500

2y>

0

x, y

0

a: Draw the feasible region of the bivarate linear program.

b: Find an optimal solution of the bivarate linear program, and calulate the

optimal year end return.

c: Write the dual program of the bivarate linear program.

d: Compute an optimal dual solution using the complementary slackness prop-

erty.

e: Complete the following three sentences using the results obtained in Parts

a-d:

If John decides to invest no more than $400 in Fund C, it is estimated that

the optimal year end return that you caculate in Part B (increases/decreases)

by

dollars at (least most).

If Fund A now offers a return of 2%, it is estimated the optimal year end

return (increases/decreases) by

dollars at (least most).

If Fund C now offers a return of 4.5%, it is estimated the optimal year end

return (increases/decreases) by

dollars at (least most).

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.