تم الحل ✓

categoryالاقتصاد والأعمال

schoolبكالوريوس

event_available2026-07-15

السؤال

Transcribed Image Text:

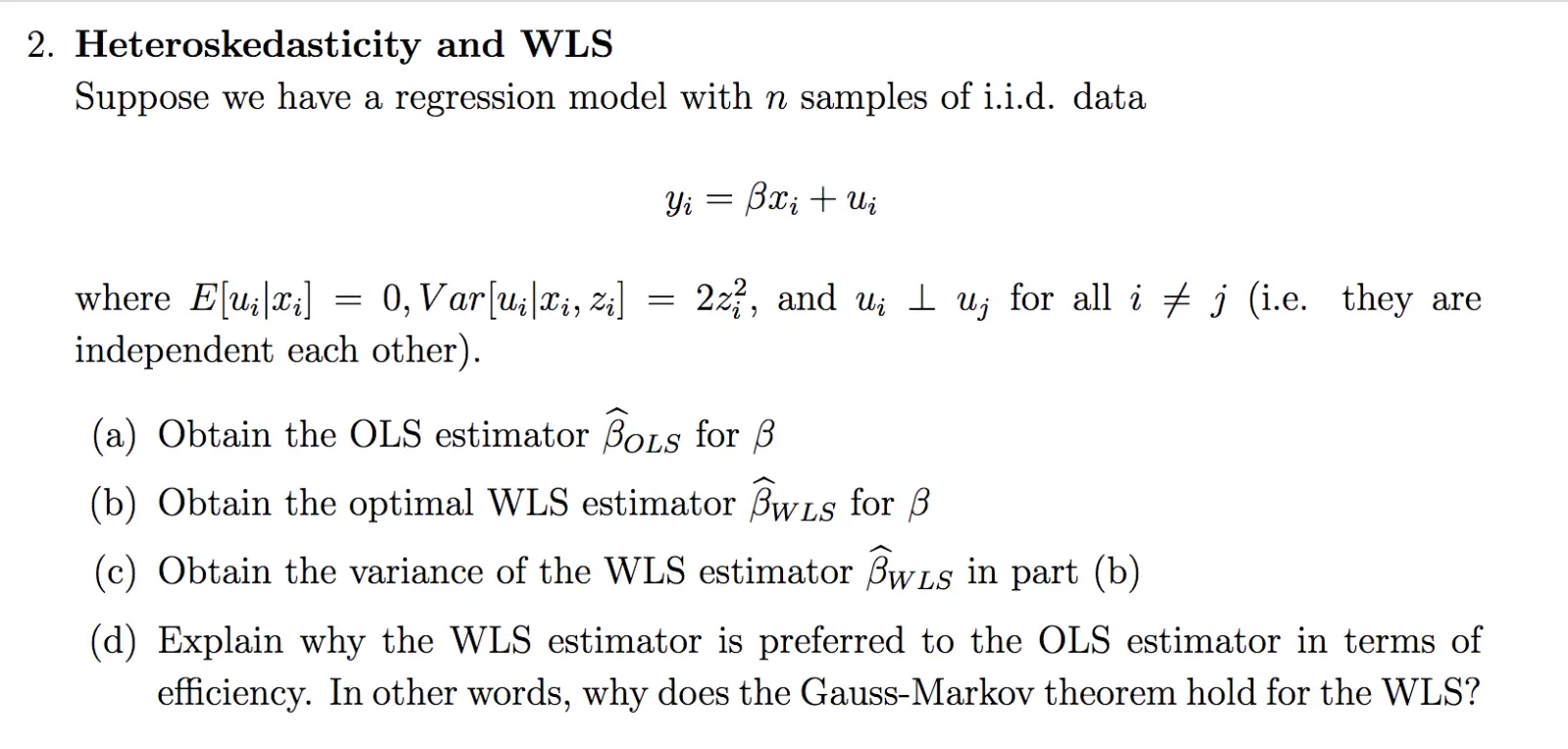

2. Heteroskedasticity and WLS

Suppose we have a regression model with n samples of i.i.d. data

where Euxi

=

0, Var[ui xi, zi]

=

independent each other).

Yi = ẞxi + ui

2z, and u u; for all i j (i.e. they are

(a) Obtain the OLS estimator BOLS for ẞ

(b) Obtain the optimal WLS estimator BWLS for ẞ

(c) Obtain the variance of the WLS estimator BWLS in part (b)

(d) Explain why the WLS estimator is preferred to the OLS estimator in terms of

efficiency. In other words, why does the Gauss-Markov theorem hold for the WLS?

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.