تم الحل ✓

categoryالاقتصاد والأعمال

schoolبكالوريوس

event_available2026-07-15

السؤال

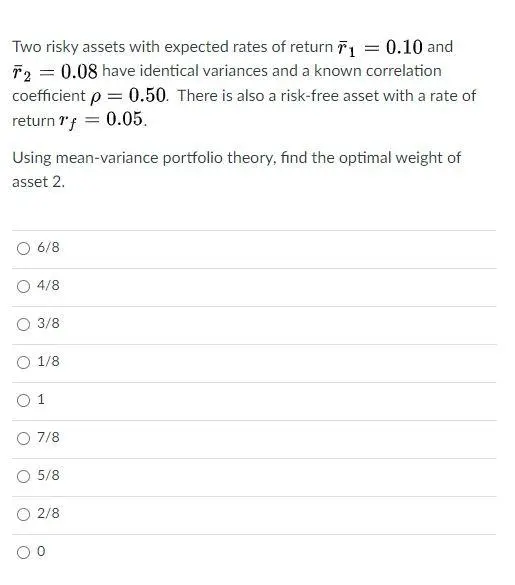

Transcribed Image Text:

O

O

Two risky assets with expected rates of return 71 = 0.10 and

T2 = 0.08 have identical variances and a known correlation

coefficient p = 0.50. There is also a risk-free asset with a rate of

return f = 0.05.

Using mean-variance portfolio theory, find the optimal weight of

asset 2.

6/8

4/8

3/8

O 1/8

F

7/8

5/8

2/8

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.