تم الحل ✓

categoryتمويل ومصارف

schoolبكالوريوس

event_available2026-07-15

السؤال

Transcribed Image Text:

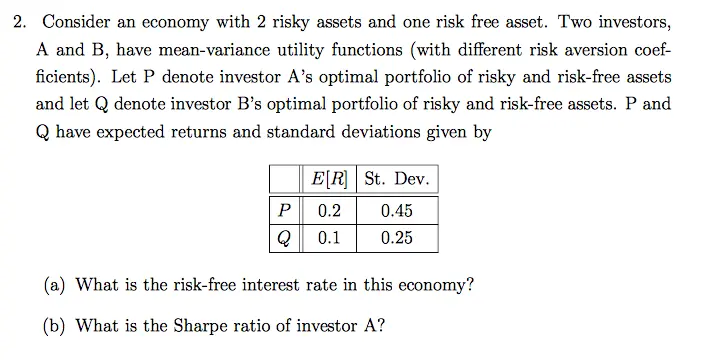

2. Consider an economy with 2 risky assets and one risk free asset. Two investors,

A and B, have mean-variance utility functions (with different risk aversion coef-

ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets

and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and

Q have expected returns and standard deviations given by

E[R] St. Dev.

P

0.2

0.45

Q

0.1

0.25

(a) What is the risk-free interest rate in this economy?

(b) What is the Sharpe ratio of investor A?

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.