تم الحل ✓

categoryالرياضيات

schoolبكالوريوس

event_available2026-07-15

السؤال

Transcribed Image Text:

-

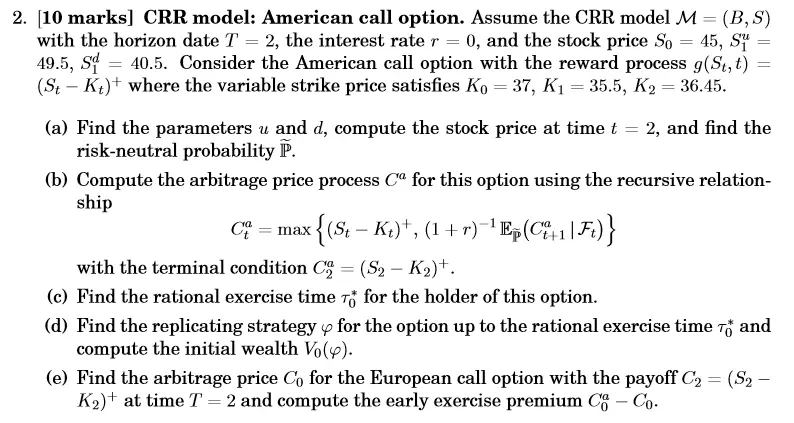

2. [10 marks] CRR model: American call option. Assume the CRR model M = (B,S)

with the horizon date T = 2, the interest rate r = 0, and the stock price So = 45, Su

49.5, Sd=40.5. Consider the American call option with the reward process g(St,t)

(StKt) where the variable strike price satisfies Ko = 37, K₁ = 35.5, K2 = 36.45.

-

(a) Find the parameters u and d, compute the stock price at time t

risk-neutral probability P.

=

=

2, and find the

(b) Compute the arbitrage price process Ca for this option using the recursive relation-

ship

C = max

ax {(St − K₁)+, (1+r)¯¹ Ep(Ci 4+1 | Ft)}

with the terminal condition C = (S2 - K2)+.

(c) Find the rational exercise time for the holder of this option.

(d) Find the replicating strategy for the option up to the rational exercise time T and

compute the initial wealth Vo(y).

(e) Find the arbitrage price Co for the European call option with the payoff C₂ = (S2 –

K2) at time T = 2 and compute the early exercise premium Co-Co.

check_circle الجواب — حل مفصل خطوة بخطوة

hourglass_top

🔒

الحل الكامل متاح للمشتركين

اشترك في أرشيف الأسئلة لعرض هذا الحل وآلاف الحلول المفصلة خطوة بخطوة من معلمين معتمدين.